Nepal’s Lending Rate Illusion

When “Base Rate + Premium” Becomes a Black Box —and why new borrowers often get better deals than loyal ones

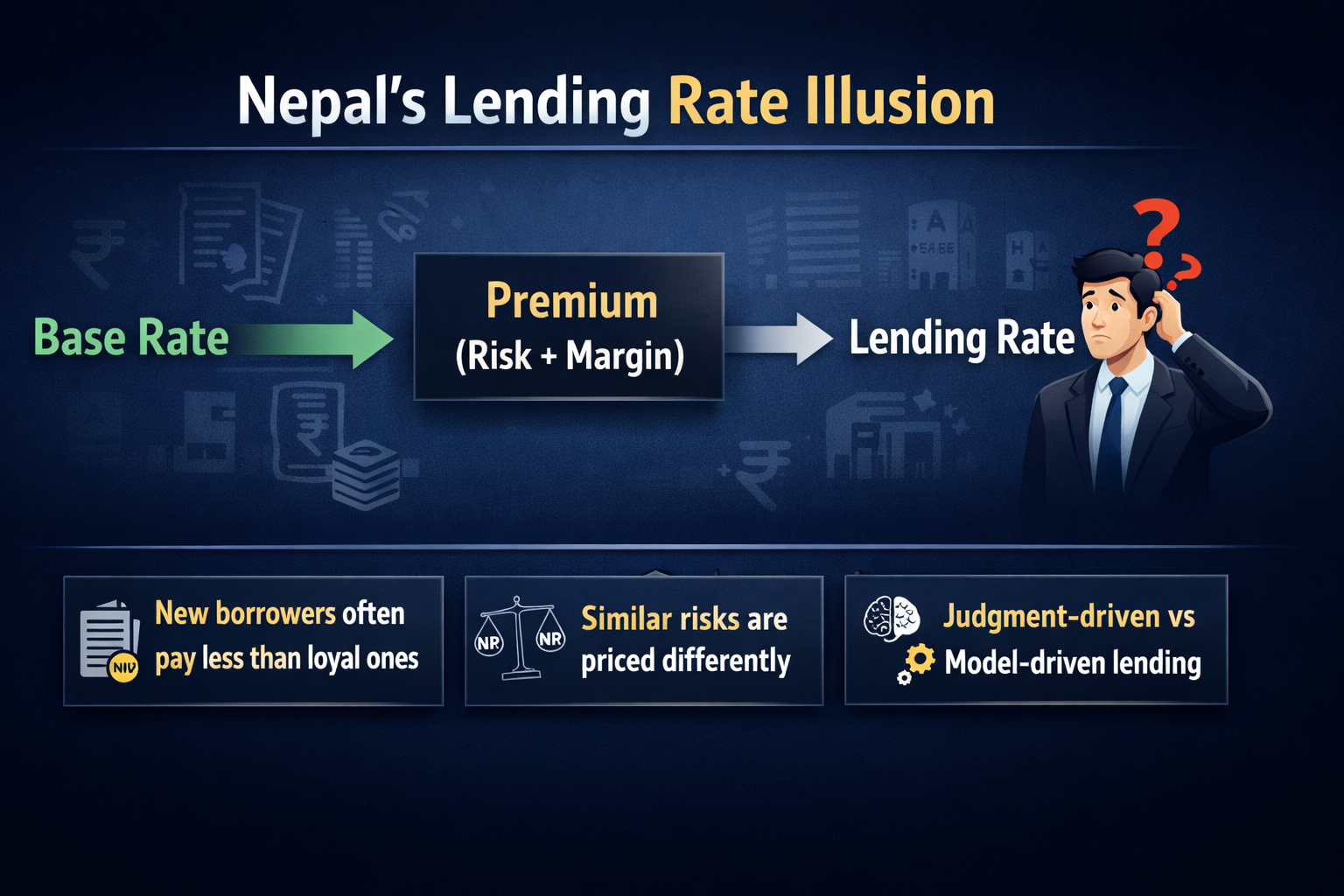

Nepal’s transition to a Base Rate + Premium lending framework—under the guidance of Nepal Rastra Bank—was designed to fix a broken past. It promised transparency, discipline, and a shift toward risk-based pricing.

On paper, the system looks modern. In practice, one critical component remains opaque: the premium.

The base rate is visible. The premium decides everything.

The Promise vs Reality

The reform was meant to follow a simple global logic: benchmark + spread = lending rate

But in Nepal:

· The benchmark is regulated

· The spread is discretionary

And that discretionary space is where opacity thrives.

Borrowers are told:

· “Your rate is Base Rate + 3%”

But rarely:

· Why 3% instead of 2% or 5%

And that “why” is the entire story.

Is the Premium Really a Black Box?

Technically, no. Practically, very close.

Banks consider:

· Default risk (repayment capacity)

· Liquidity and recovery conditions

· Loan tenure

· Sector exposure

But these factors are rarely:

· Standardized

· Clearly disclosed

· Auditable from a borrower’s perspective

What should be risk-based pricing often feels like negotiated pricing.

When pricing logic is invisible, trust becomes negotiable.

The Collateral Comfort Zone

Despite policy intent, Nepal has not fully transitioned to cash-flow-based lending.

Premiums still lean heavily on:

· Land and building valuation

· Personal guarantees

· Relationship history

This creates a structural distortion:

· Asset-rich but low-productivity borrowers get cheaper loans

· High-potential but asset-light entrepreneurs pay more

That is not risk pricing. That is risk avoidance.

Same Risk, Different Price

In mature systems, similar borrowers converge toward similar rates.

In Nepal:

· Two comparable SMEs can face very different premiums

· Even within the same bank, pricing varies across branches

This is not just flexibility—it signals something deeper:

The system is still personality-driven, not model-driven.

The Paradox: New vs Existing Borrowers

A striking anomaly is emerging in today’s liquidity-rich environment.

Banks are:

· Offering new borrowers loans near the base rate to gain market share

· Continuing to charge existing borrowers higher premiums—even with proven repayment records

Illustration:

· Existing borrower → 5% + 3.5% = 8.5%

· New borrower → 5% + 1% = 6%

The paradox is clear: The proven borrower pays more than the untested one.

Why this happens:

· Aggressive credit growth strategies

· Switching inertia among existing clients

· Incentive structures that reward new disbursement, not portfolio fairness

The premium, therefore, becomes not just a risk tool—but a strategic pricing lever.

The Policy Transmission Gap

When Nepal Rastra Bank adjusts monetary policy:

· Base rates adjust slowly due to deposit stickiness

· Premiums often remain unchanged

The result:

· Delayed transmission

· Partial impact on borrowers

Policy signals weaken before they reach the real economy.

Why Banks Defend the System

Banks are not acting irrationally.

They operate within constraints:

· Weak credit information systems

· Lengthy legal recovery processes

· Economic volatility

· Informal financial behavior

In this environment, the premium becomes:

A buffer against uncertainty the system has not yet solved.

The Real Cost of Opacity

This is not just a technical flaw—it shapes the economy:

· Businesses struggle to predict borrowing costs

· Financial planning becomes conservative

· Credit demand weakens during uncertainty

· Trust in the financial system erodes

Over time, this directly affects:

· Investment decisions

· SME growth

· Financial inclusion

What Needs to Change

Not more regulation—better clarity.

1. Structured Premium Disclosure Borrowers should see:

· Credit risk contribution

· Tenure impact

· Collateral adjustments

2. Standardized Risk Bands

· Low / Medium / High risk categories

· Indicative premium ranges

3. Stronger Credit Infrastructure Shift toward data-driven lending:

· Cash flow analysis

· Digital transaction history

· Sectoral benchmarks

4. Internal Pricing Discipline

· Reduce branch-level subjectivity

· Strengthen model-based pricing frameworks

Final Reflection

Nepal’s lending rate system is not broken. It is unfinished.

· The base rate brought transparency

· The premium still operates in shadow

· And today, new borrowers can pay less than proven ones

Until the premium becomes explainable, consistent, and fair, lending will remain only partially transparent.

And in finance, partial transparency is simply a more sophisticated form of opacity.